Industrial printer shipments declined 1.6% year over year in the second quarter of 2022 (2Q22), according to new data from the International Data Corporation (IDC) Worldwide Quarterly Industrial Printer Tracker.

“The worldwide market is still hindered by supply chain challenges and other disruptive global events,” said Tim Greene, research director, Hardcopy Solutions at IDC. “While we’re seeing some really strong developments that indicate strength on the demand side, the availability of products across the board is still questionable, and that is a factor for the industrial printer market in 2022.”

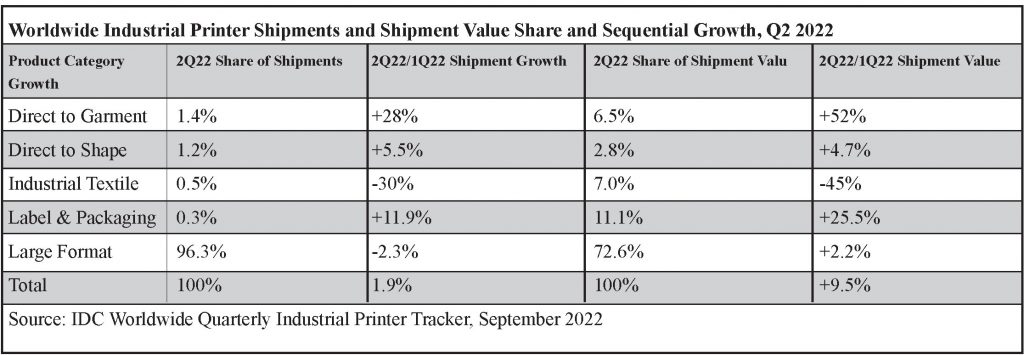

Q2 2022 Highlights

• Large format digital printer shipments declined almost 2.5% on a worldwide basis compared to Q1 2022.

• Direct-to-garment (DTG) printer shipments grew 22% in 2Q22 when compared to the previous quarter. Higher end unit growth drove solid gains in system value.

• Direct-to-shape printer shipments grew 5.2% in 2Q22 compared to 1Q22.

• Industrial digital label & packaging printer shipments grew 10.6% compared to the previous quarter.

• Industrial textile printer shipments declined 28% compared to 1Q22.

Regional Analysis

“More than any particular industry or technology segment the changes in regional markets were what drove total shipments lower for the quarter,” noted Greene. Regional results for 2Q22 include the following highlights:

• Shipments in the Central & Eastern European market were down nearly 45% as more global vendors limit their activities in the region due to the war in the Ukraine.

• Shipments in China declined by 17% compared to 1Q22 while shipments in Japan declined by 13% compared to 1Q22.

• Shipments in North America (US + Canada) grew more than 12% compared to the previous quarter.

• Modest growth in Western Europe, Latin America, and the Middle East & Africa regions helped offset some of the declines in other regions.

Outlook for the Second Half of 2022: Uncertainty continues to be the dominant theme in the industrial printer market. Although many of the global supply chain issues improved in the second quarter, global events are still impacting the industry. In addition to any lingering supply chain problems, inflation and a potential recession continue to cloud the outlook for the second half of 2022 and beyond. However, many of the demand drivers are positive and that has helped offset some of the market disruption caused by these global concerns.

IDC’s Worldwide Quarterly Industrial Printer Tracker provides total market size and vendor share for five major market categories: large format, label and packaging, direct to garment, industrial textile, and direct to shape. In addition to units, shipment value, and average selling price (ASP), the Tracker also provides market results for each product category by ink type, media size, hardware class, or primary application across nine geographic regions and 90 countries.

About IDC Trackers: IDC Tracker products provide accurate and timely market size, vendor share, and forecasts for hundreds of technology markets from more than 100 countries around the globe. Using proprietary tools and research processes, IDC’s Trackers are updated on a semiannual, quarterly, and monthly basis. Tracker results are delivered to clients in user-friendly Excel deliverables and on-line query tools.

About IDC: International Data Corporation (IDC) is the premier global provider of market intelligence, advisory services, and events for the information technology, telecommunications, and consumer technology markets. With more than 1,300 analysts worldwide, IDC offers global, regional, and local expertise on technology, IT benchmarking and sourcing, and industry opportunities and trends in over 110 countries. IDC’s analysis and insight helps IT professionals, business executives, and the investment community to make fact-based technology decisions and to achieve their key business objectives.